The biggest secret in freight forwarding? The margins look small until you understand capital velocity.

One of the funniest things about freight forwarding is how many people underestimate the business from the outside. They hear a forwarder made $150 on an airfreight shipment from Hong Kong to Frankfurt and immediately think, “That’s it?” What they don’t see is the velocity.

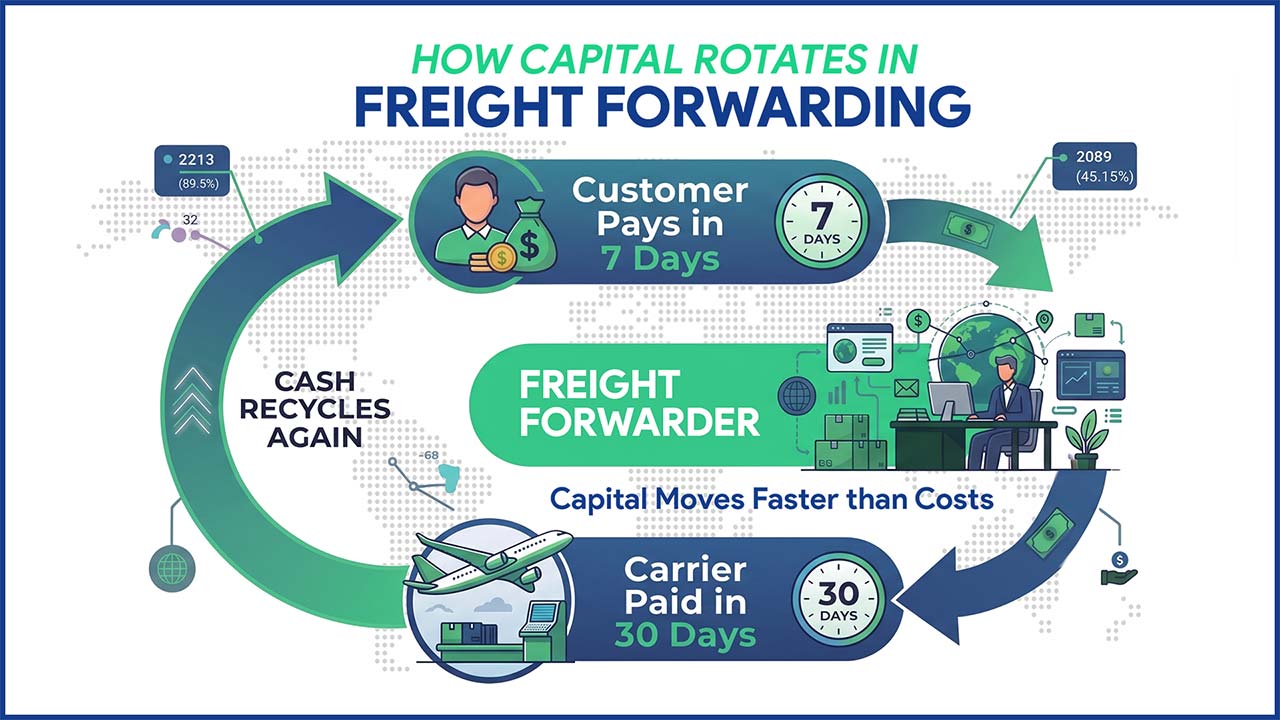

Freight forwarding is not really a margin business. It is a capital velocity business disguised as a service industry, and that difference changes everything.

Take a simple airfreight shipment. A forwarder moves 500 kilos of electronics from Hong Kong to Germany. The shipment sells for $4,000, while the airline, handling, and origin costs total $3,700. The forwarder earns a gross profit of $300. To most people, $300 sounds unimpressive.

But now let’s look deeper.

The customer pays the forwarder within 7 days, while the airline and suppliers provide 30-day payment terms. That means the forwarder recovers cash long before the carrier invoice is even due.

Now, imagine the forwarder only needs around $20,000 in working capital to continuously operate this lane because the money keeps circulating back quickly. If that same capital rotates just twice per week across multiple shipments, the numbers become interesting very fast.

Let’s say the company handles 10 similar airfreight shipments per week, earning $300 gross profit per shipment across 50 working weeks per year. That equals $3,000 gross profit per week, or $150,000 gross profit annually.

Now compare that to the original working capital requirement of roughly $20,000.

Suddenly, the forwarder is generating returns that many traditional industries would envy. Not because of huge margins. Not because they own aircraft. Not because they invested millions into factories. But because the same capital keeps moving rapidly through the system.

That is the hidden engine of forwarding.

The smartest freight forwarders are not obsessed with maximizing one transaction. They focus on increasing trust, shipment frequency, customer retention, and trade lane stability. One lane becomes predictable. Predictability creates volume. Volume increases capital velocity. Capital velocity compounds returns.

And unlike many industries, freight forwarding sits directly in the bloodstream of global commerce. Every delayed shipment creates urgency. Every factory shortage creates demand. Every supply chain disruption creates opportunities for the forwarder who can solve problems faster than competitors.

That is why the business remains incredibly resilient despite constant market changes and new technology entering the industry. Because forwarding is still deeply human.

When cargo gets stuck somewhere in the world at 2 a.m., customers are not searching for an app. They are calling someone they trust.

Ironically, this is why freight forwarding often hides its profitability so well from outsiders. People only look at the margin on one shipment. Experienced operators look at how many times trust, cargo, and capital can rotate together in one year.

That is where the real money is made.